This has historically been a time for lumber prices to start dropping as the season changes to autumn. Generally speaking, construction activity starts to slow down after Labour Day.

For the past year of rising interest rates and some unknowns for the housing market, lumber buyers have kept their inventories lean due to uncertainty of consistent demand. With industry folks this is known as just-in-time buying. The strategy can fail if there is a sudden increase in lumber sales but not enough inventory in the field to serve that rise in demand.

At the moment, the sawmills have been running at less-than-optimal capacity utilization rates, so customers have felt confident they would not get caught short without the wood they need for ongoing projects. If demand increased suddenly, lumber manufacturers could simply increase production to sell higher volumes while keeping the price relatively even.

In this wait-and-see environment, some lumber prices have popped up slightly. Prompt availability was increasingly difficult to come by. Suppliers with readily available material that could be shipped in a timely manner were highly sought after.

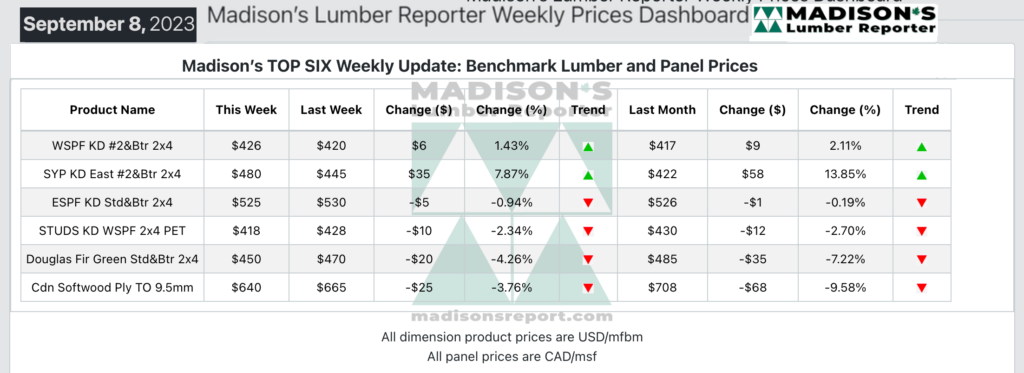

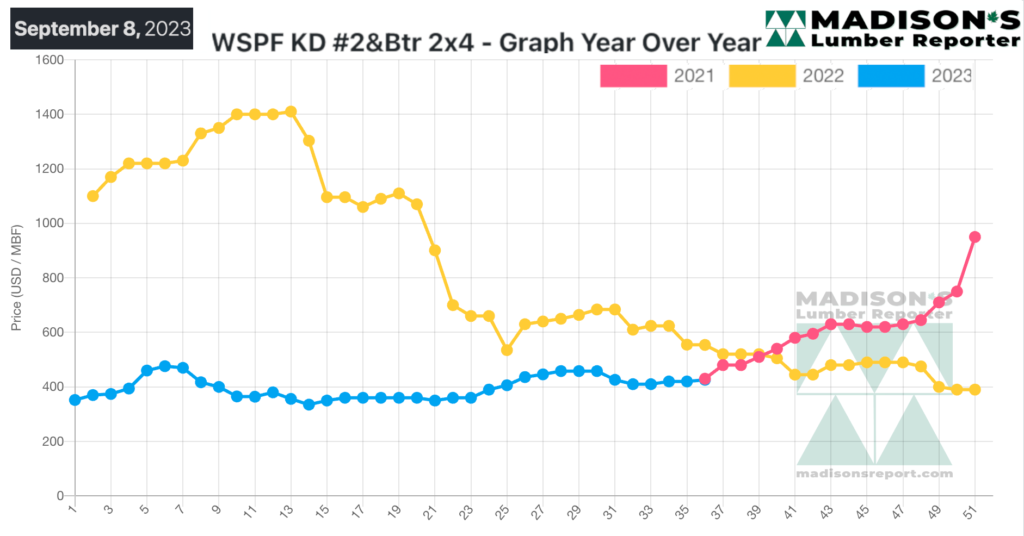

In the week ending September 8, 2023, the price of benchmark softwood lumber item Western Spruce-Pine-Fir 2×4 #2&Btr KD (RL) was US$426 mfbm. This is up by +$6, or +1%, compared to the previous week when it was $420, said weekly forest products industry price guide newsletter Madison’s Lumber Reporter.

That week’s price is up by +$9, or +2%, from one month ago when it was $417.

SPF lumber and studs sellers reported a tone of quietude, belied by sneaky strong inquiry and sales activity. Prices of panel products continued to erode in search of tradable levels.

Purveyors of Western S-P-F lumber and studs in the United States described a steadily strengthening market. The deep counter offers of early August faded away and players reported improving liquidity most days. One experienced wholesaler related their position: really busy but not investing in the future.

Sales of studs were a mixed bag, with demand for eight-footers showing strength while sales of 2×4- and 2×6-10’s have been soft for weeks.

The trend in that latter trim was apparently caused by a shift in home construction to smaller and shorter builds as a cost-cutting measure in response to elevated material prices, interest rates, and inflation numbers.

Western S-P-F lumber suppliers in Western Canada were busy with customers on both sides of the border. Buyers remained circumspect when it came to longer coverage even as repeat just-in-time business was healthy and consistent.

This sustained strategy begat thin field inventories across the board, as has been the case throughout August so far. Sales of bread-and-butter narrows were the strongest, particularly 2×4 R/L premium and standard grade. Meanwhile, the ongoing catastrophic wildfires in BC – and across virtually all of Southern Canada – continued to foster a sense of unease in reference to long-term supply.

Prices of Western S-P-F studs gained some modest ground, with bread-and-butter trims firm or slightly up from the previous week’s levels. Demand was expanded to covering more than just immediate needs in many cases, as downward pressure dissipated and customers decided to secure material into the month of September. Mid-September order files were established by Western Canadian stud mills, thus successful counter offers dried up. Transportation remained surprisingly smooth according to players, with multiple freight movers competing for loads.

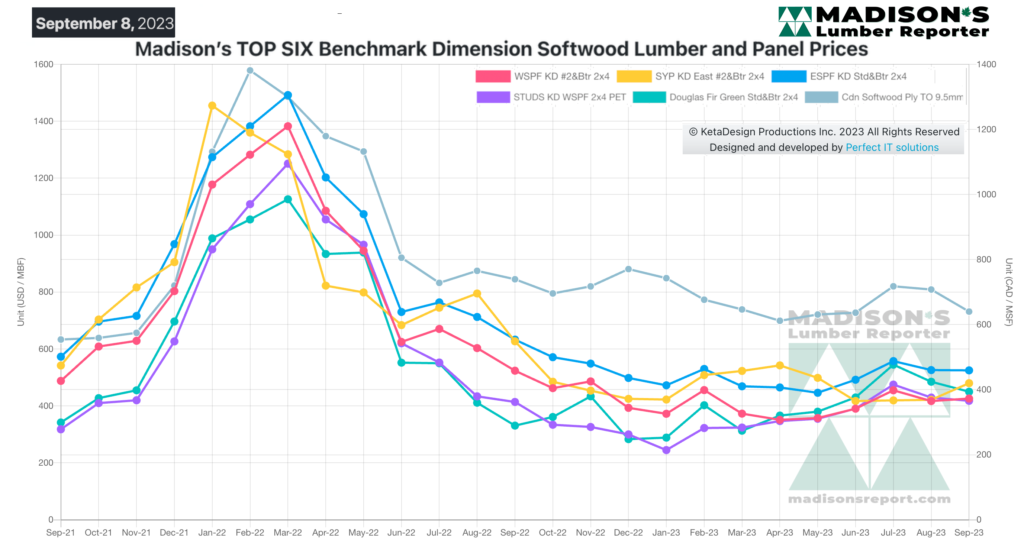

Madison’s Benchmark Top-Six Softwood Lumber and Panel Prices: Monthly Averages