Even in the middle of May the usual spring home construction did not materialize.

The harsh winter was a distant memory as normal seasonal weather was upon North America, yet building activity did not increase. Whether it was concerns over macroeconomic conditions, questions about potentially low new home sales, or simply uncertainty in general; most players were staying on the sidelines with their lumber purchases. It seemed like everyone was waiting to see what everyone else would do.

Meanwhile, the wildfires in Alberta were somewhat reduced however still very serious.

It turns out that about half those forest fires were caused by human activity, which is incredibly disappointing; specifically because those could have been avoided.

At this time in mid-May those fires burned almost 900,000 hectares of Alberta forests.

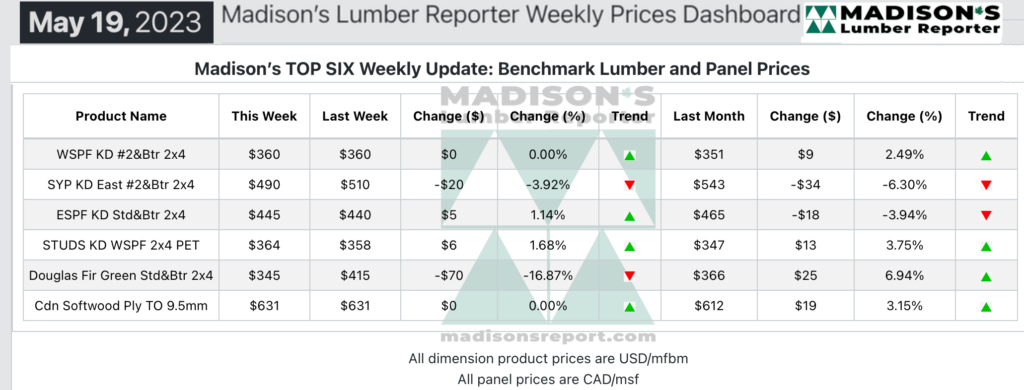

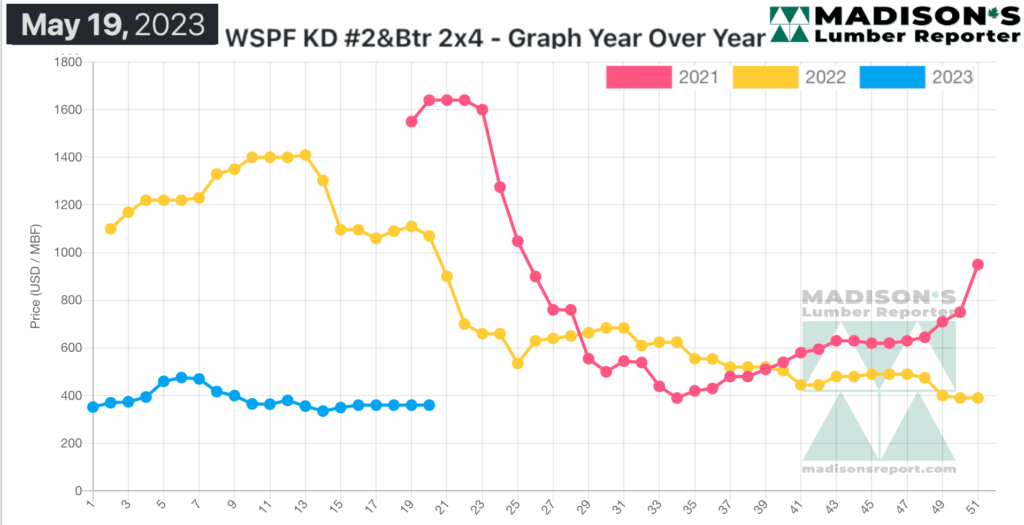

In the week ending May 19, 2023, the price of Western Spruce-Pine-Fir 2×4 #2&Btr KD (RL) was US$360 mfbm, which is flat from the previous week, said weekly forest products industry price guide newsletter Madison’s Lumber Reporter.

That week’s price is up by +$9, or +2%, from one month ago when it was $351.

Buyers were still extremely hesitant to take long positions and instead kept to short-covering, leading to perpetually-low field inventories.

Wildfires in Western Canada were top of mind while the broader North American solid wood commodities market continued to stumble slowly into mid-Spring.

Sales activity remained atypically lukewarm for the time of year according to Western S-P-F traders in the United States.

Most players agreed that the upcoming Victoria Day and Memorial Day holiday weekends in Canada and the US respectively will be the next crucial litmus test for the North American lumber market.

For their part, US sawmills established order files around two weeks out, but many regional facilities continued to show prompt availability on certain widths and trims.

Steady inquiry and takeaway from industrial buyers kept low grade material moving.

Wildfires continued to be a main topic of conversation this week among Western Canadian S-P-F lumber traders. Many thousands more residents were forced from their homes as ongoing hot and dry conditions fuelled blazes across much of Western Canada, particularly in Alberta. Recent sawmill curtailment announcements added another looming question mark to the state of supply.

Even though buyers remained circumspect and sales volumes were still lacklustre for the time of year, promising signs of increasing future demand were evident. Transportation appeared to be smooth for the time being, as forest fires haven’t closed any major highway routes as yet. There were pockets of slow-moving freight in Alberta due to the blazes, however.

Traders of Southern Yellow Pine were beginning to sound like broken records. Prices of narrow dimension R/L items were almost identical to last week, while 2×12 remained the strongest seller and most scarce commodity. Demand for SYP MSR was hopping as truss producers were busier with each passing week. Sales of low grade showed some hustle as that category has been tight in supply lately..

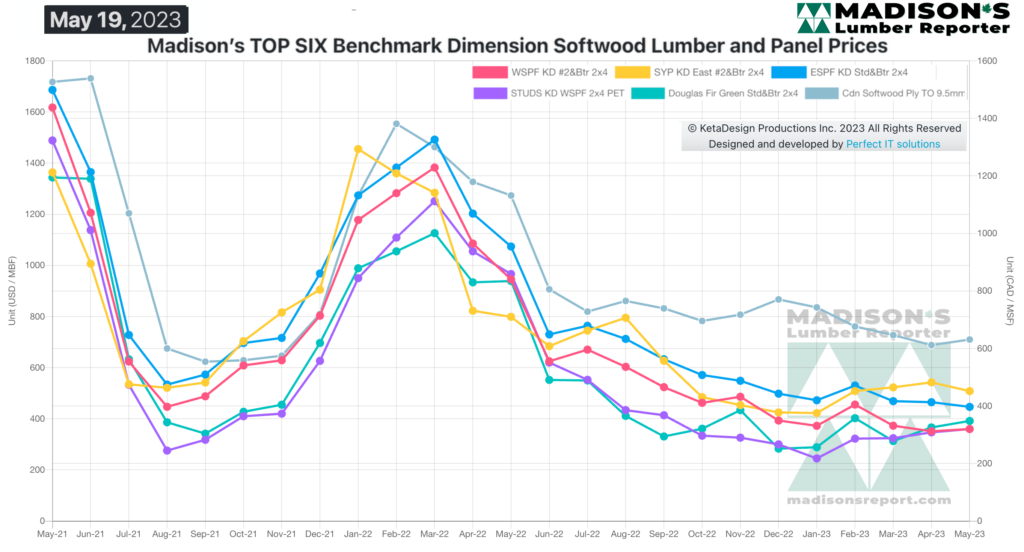

Madison’s Benchmark Top-Six Softwood Lumber and Panel Prices: Monthly Averages