Toward the end of August the recent increases in construction framing dimension softwood lumber prices slowed somewhat, while that of plywood and OSB did pop a little bit.

Demand at sawmills and secondary suppliers increased noticeably, causing sellers to wonder if this was just a momentary blip or if higher sales volumes would carry through the Labour Day long weekend.

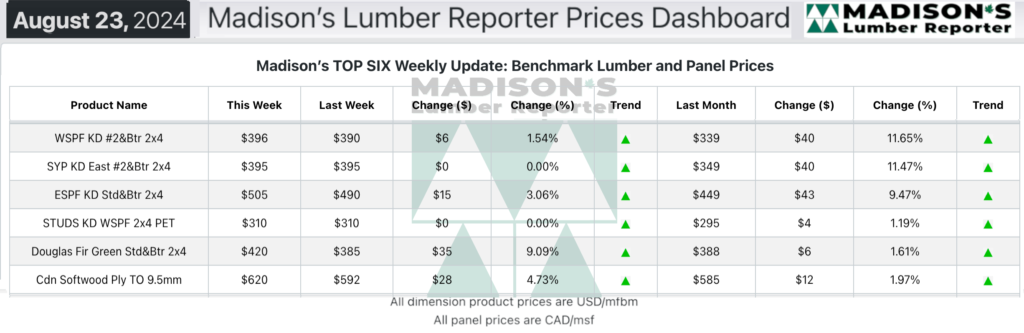

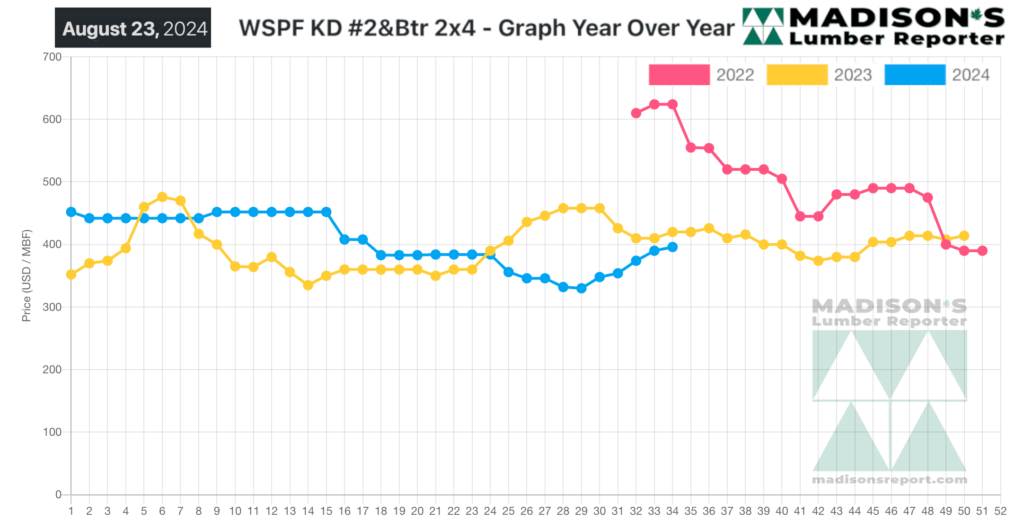

For the time being it seemed like a bit of an equilibrium had been reached, as benchmark Western S-P-F KD 2×4 #2&Btr prices approached quite close to where they had been in the same week last year.

Does this indicate a stability finally arriving for the lumber manufacturing industry? Given that the data shows the price bottom was reached and surpassed in mid-July this year, it

does seem that a form of supply-demand balance has been achieved.

Once the all-important Labour Day long weekend has been passed, confirmation of this will be possible.

In the week ending August 23, 2024, the price of Western Spruce-Pine-Fir 2×4 #2&Btr KD (RL) was US$396 mfbm, which is up +$6, or +2%, from the previous week when it was $390, said weekly forest products industry price guide newsletter Madison’s Lumber Reporter.

That week’s price is up +$57, or +17%, from one month ago when it was $339.

The Canada-wide rail strike dominated the conversation this week. Dimension items continued to strengthen, led by 2×6 and 2×12 in most cases.

KEY TAKE-AWAYS:

- Purveyors of Western S-P-F in the United States described a supply-driven tack to business.

- Secondary suppliers noted that volumes sold in half the time, as was the case in recent months.

- Supply of Eastern S-P-F was a worry going forward, with most customers’ inventory only covered for the next 30 days or so.

- There was quiet discounting on certain widths and lengths of Southern Yellow Pine as sawmills tried to keep the flow of material moving.

- Buyers of green Douglas Fir were busier than they have been in months.

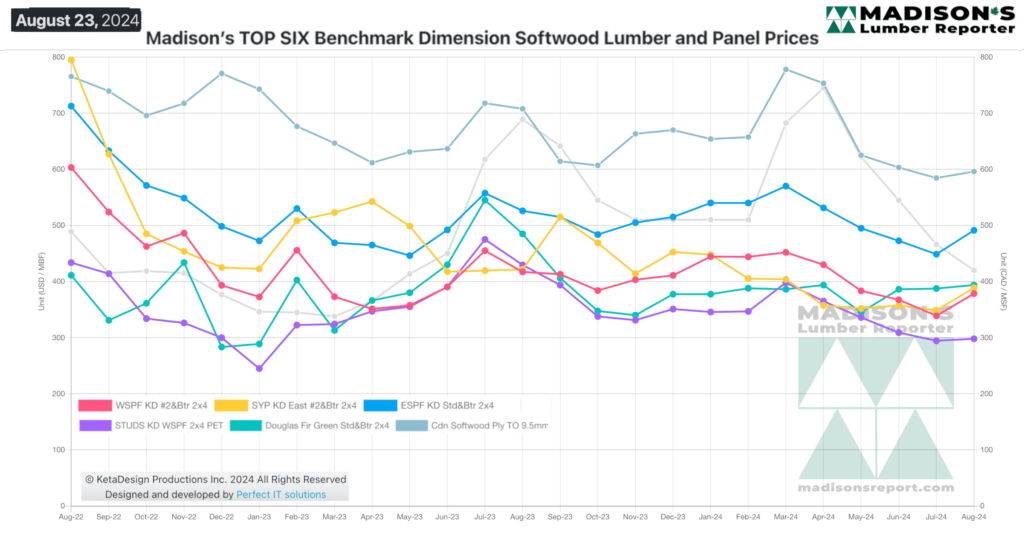

Madison’s Benchmark Top-Six Softwood Lumber and Panel Prices: Monthly Averages