Even as February US and Canadian housing starts data showed big increases over January and positive growth over February 2022, lumber buyers across North America remained cautious toward the end of March.

Customers continued their habit of making only highly-specified orders of wood they needed for existing projects; still at this time there was no inventory building or stocking up.

Suppliers were not in a position to complain as they picked through their lumber yards to provide these custom-requested tallies.

All looked forward to true spring weather and the start of construction season.

If this latest new home building data is any indication,

rightfully expectations should be that this year will be a good one for residential construction.

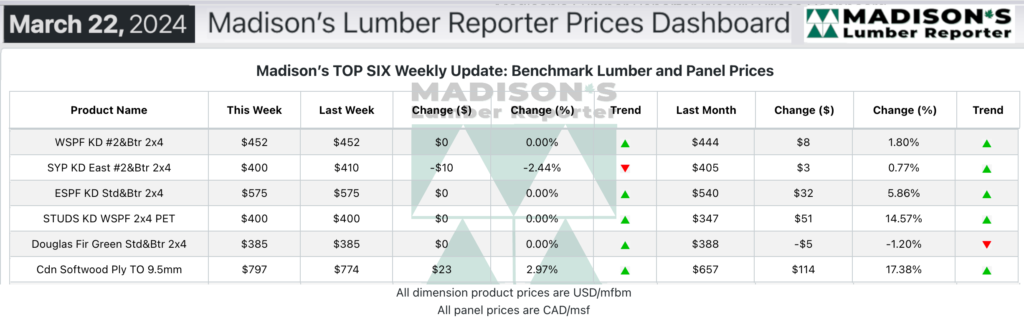

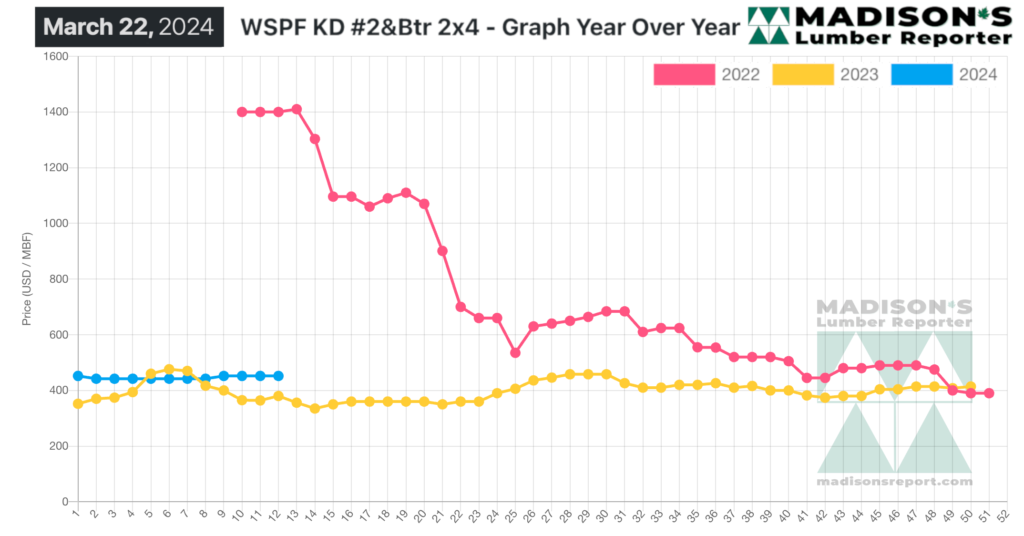

In the week ending March 22, 2024, the price of benchmark softwood lumber item Western Spruce-Pine-Fir 2×4 #2&Btr KD (RL) was US$452 mfbm. This is flat compared to the previous week when it was $452, said weekly forest products industry price guide newsletter Madison’s Lumber Reporter.

That week’s price is up by +$8, or +2%, from one month ago when it was $444.

Panel prices jumped yet again. Most lumber buyers having covered their most pressing needs and balking at current price lists, that market entered a digestion phase.

Having built comfortable order files into April amid firm asking prices, Spruce-Pine-Fir sawmills out West were unwilling to wheel and deal on any orders. Inventories at supplier yards were almost as patchy as those in the field. For now, the gambit of relying on secondary suppliers to have quickly available material on hand appeared to be paying off. Some sawmills started to show availability of items that had been off the market last week, which indicated a potential shift in the supply-demand balance..

Demand and availability of Southern Yellow Pine varied considerably from item-to-item. Buyers did their best to stand pat while waiting for the spring sales surge to arrive. Inquiry and follow-through were largely region-dependent, with the Western zone the most active.

Price levels on both OSB and plywood continued to surge as order files with producers were into the end of April. Buyers went into a digestion retreat even while overall supply remained low.

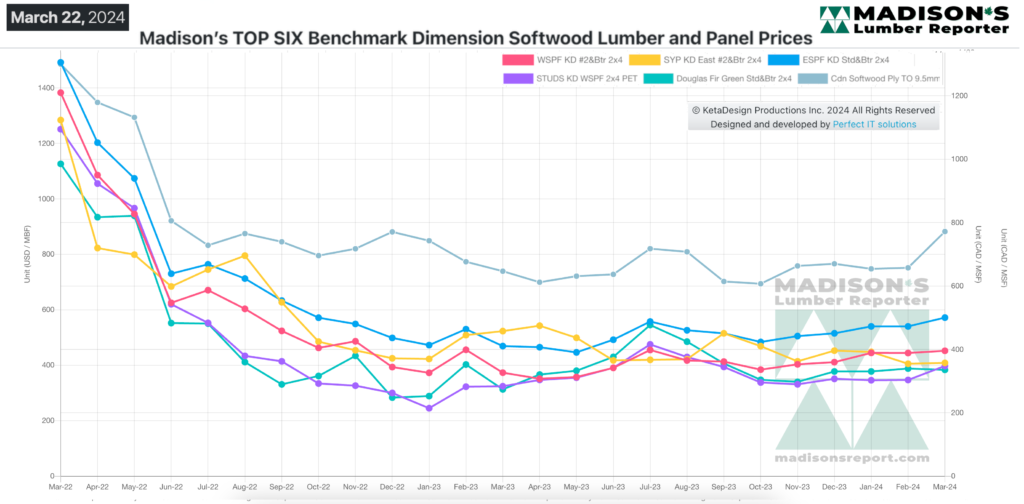

Madison’s Benchmark Top-Six Softwood Lumber and Panel Prices: Monthly Averages